India Unified Payments Interface has become the backbone of digital payments by enabling wide range of transaction types with faster response time and security. The core functionality of UPI are Peer-to-Peer Transfers and Recurring Mandates. each are specific payment workflows for user needs.

This is the second chapter of the UPI blog series. You can find the links to the other chapters at the end of this blog. In this blog we will take a deep dive into the technical aspects of how UPI handles P2P Transfers and we will also cover evolution of Recurring Mandates and how UPI Autopay beat all other Mandates types.

Peer-to-Peer Transfers

UPI enables flexible payment modes for seamless transactions. Users can transfer funds using a UPI ID (Virtual Payment Address) without sharing bank details. Payments can also be made by scanning QR codes, ideal for purchases or peer-to-peer transfers. Additionally, sending money via a registered mobile number linked to a UPI ID simplifies the process further.

Types of UPI Payment Mode

1. Collect Payment — Collect Payment in UPI allows users to request money by sending a payment request to the payer’s UPI ID. The payer approves the request using their UPI app, ensuring secure and convenient fund transfers.

Common for bill payments, peer-to-peer transfers, or merchant transactions where the recipient generates a payment request.

2. Intent Payment — Intent Payment in UPI enables seamless transactions by directly invoking a UPI app from a merchant’s app, website, or QR code. Users can scan the QR code or interact with the app link, simplifying the process to approve payments instantly within their preferred UPI app.

Typically involves scanning a QR code or entering the merchant’s VPA for point-of-sale payments or online purchases.

Recurring Mandates

The evolution of mandates in the payments ecosystem especially for recurring payments has progressed through several stages each enhancing the previous method to offer smoother more secure and scalable solutions.

In this overview we will briefly introduce SI on card, NACH, e-NACH, and UPI AutoPay followed by a detailed exploration of UPI Autopay.

1. Standing Instruction (SI) on Card

Standing Instructions on card allow payments to be automatically charged to credit / debit card at regular intervals. i.e. daily, monthly or annually. Card holders authorize the merchant to charge a fixed amount on their card for the duration of the service.

Limitations:

Customer may not be able to manage or cancel standing instructions easily especially if they forget about it. Can lead to unexpected charges if the customer loses track of the service or the terms change.2. NACH — National Automated Clearing House

NACH is centralized platform managed by the NPCI which facilitates recurring payments. NACH was primarily used for bank to bank transfer including direct debit mandates for recurring payments i.e. loan EMIs, utility bill payments etc.

Limitations:

NACH mandates were traditionally manual paper based process, requiring customers to physically sign a form at their bank. The process could be slow and cumbersome sometime due to the physical paperwork and need for bank approval.3. e-NACH — Electronic National Automated Clearing House

e-NACH is the digital version of NACH which allows card holders to authorize payments electronically via issuing bank’s internet banking or mobile banking app. The customer authorizes recurring payments by digitally signing a mandate using their bank account credentials usually via OTP, Net banking or other secure channels.

Limitations:

Not universally adopted across all services although it is growing in popularity especially for bank-to-bank transactions. Some customers may still find it challenging to authenticate or manage their mandates digitally.4. UPI AutoPay

In India UPI AutoPay is a recent and revolutionary addition to the recurring payment landscape based on the UPI as backend system . UPI AutoPay enables customers to authorize recurring payments via their VPA making it a simple and seamless way to manage payments for services like subscriptions, recharges, and other recurring bills.

It was introduced by NPCI to enable safer, quicker and more accessible recurring payments using UPI without the need for cards or traditional bank mandates.

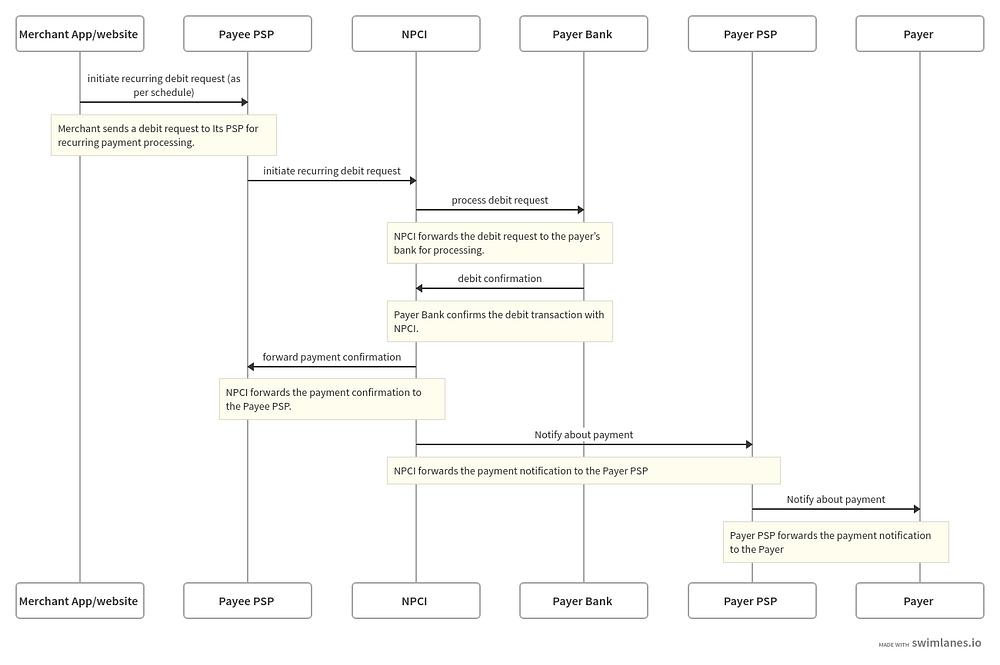

The UPI AutoPay system flow can be categorized into two parts: Mandate registration and Next auto payment

a. Mandate registration

Let’s understand the UPI Mandate registration process using an example. Suppose a user subscribes to a Netflix plan with a recurring monthly payment.

Netflix sends a request to the user’s PSP to create a UPI mandate for the subscription.

The user reviews the mandate details and authorizes it by entering their UPI PIN.

Finally, the payer’s PSP submits the mandate to NPCI, which processes the authorization and confirms the setup.

b. Next payment

On the due date Netflix will automatically debit the user’s bank account for the subscription amount. The UPI AutoPay system ensures the payment is processed seamlessly without requiring further user intervention.

In this chapter, we explored the types of payments that UPI facilitates. In the next chapter, we will dive into how payment settlement works within the UPI ecosystem.

Thank you for reading! Your feedback is always appreciated.

Chapter 3: Payment SettlementChapters

Chapter 1 : A Seamless Payment Revolution architecture and its core components, understanding the mechanisms that enable millions of transactions to happen in real time. Chapter 2 : Payment Types Peer-to-Peer Transfers and Recurring Mandates. Chapter 3: Payment Settlement the Settlement processes, and UPI’s inner workings.